Is there a method in numpy for calculating the Mean Squared Error between two matrices?

I’ve tried searching but found none. Is it under a different name?

If there isn’t, how do you overcome this? Do you write it yourself or use a different lib?

![]()

asked May 27, 2013 at 13:59

![]()

4

You can use:

mse = ((A - B)**2).mean(axis=ax)

Or

mse = (np.square(A - B)).mean(axis=ax)

- with

ax=0the average is performed along the row, for each column, returning an array - with

ax=1the average is performed along the column, for each row, returning an array - with omitting the ax parameter (or setting it to

ax=None) the average is performed element-wise along the array, returning a scalar value

9

This isn’t part of numpy, but it will work with numpy.ndarray objects. A numpy.matrix can be converted to a numpy.ndarray and a numpy.ndarray can be converted to a numpy.matrix.

from sklearn.metrics import mean_squared_error

mse = mean_squared_error(A, B)

See Scikit Learn mean_squared_error for documentation on how to control axis.

answered Apr 3, 2016 at 16:17

![]()

Even more numpy

np.square(np.subtract(A, B)).mean()

answered Nov 19, 2017 at 8:11

![]()

Mark SwardstromMark Swardstrom

17.2k6 gold badges62 silver badges70 bronze badges

1

Just for kicks

mse = (np.linalg.norm(A-B)**2)/len(A)

![]()

desertnaut

57.7k27 gold badges140 silver badges167 bronze badges

answered Jun 16, 2020 at 6:26

![]()

Another alternative to the accepted answer that avoids any issues with matrix multiplication:

def MSE(Y, YH):

return np.square(Y - YH).mean()

From the documents for np.square:

Return the element-wise square of the input.

![]()

desertnaut

57.7k27 gold badges140 silver badges167 bronze badges

answered Aug 31, 2017 at 16:04

The standard numpy methods for calculation mean squared error (variance) and its square root (standard deviation) are numpy.var() and numpy.std(), see here and here. They apply to matrices and have the same syntax as numpy.mean().

I suppose that the question and the preceding answers might have been posted before these functions became available.

Remarks on statistics

To answer the comment made by @Drew :

This answer is equivalent to the top answers in this thread. Technically, MSE differs from variance in that it uses «true» value of the parameter, rather than its estimate, see

What’s the difference between the variance and the mean squared error? and What is the Difference between Variance and MSE?. The two quantities then differ by the bias of our estimate of the central parameter. However, when calculating sample variance, as is done in the OP, we cannot really know the value of this parameter. I believe the OP uses term MSE in a loose sense.

Furthermore, the numpy functions proposed above allow for parameter ddof (the number of degrees of freedom), which allows to obtain unbiased variance estimates (contrary to what is claimed in some superficial comparisons between python and R.)

answered Oct 12, 2020 at 9:58

![]()

Roger VadimRoger Vadim

3732 silver badges12 bronze badges

1

What about this to keep with the np.operation style?

mse = np.mean(np.square(A - B))

Just keep in mind that np.mean() with no axis keyword argument specified will output a scalar, just like np.sum().

answered Mar 1 at 6:37

![]()

Is there a method in numpy for calculating the Mean Squared Error between two matrices?

I’ve tried searching but found none. Is it under a different name?

If there isn’t, how do you overcome this? Do you write it yourself or use a different lib?

![]()

asked May 27, 2013 at 13:59

![]()

4

You can use:

mse = ((A - B)**2).mean(axis=ax)

Or

mse = (np.square(A - B)).mean(axis=ax)

- with

ax=0the average is performed along the row, for each column, returning an array - with

ax=1the average is performed along the column, for each row, returning an array - with omitting the ax parameter (or setting it to

ax=None) the average is performed element-wise along the array, returning a scalar value

9

This isn’t part of numpy, but it will work with numpy.ndarray objects. A numpy.matrix can be converted to a numpy.ndarray and a numpy.ndarray can be converted to a numpy.matrix.

from sklearn.metrics import mean_squared_error

mse = mean_squared_error(A, B)

See Scikit Learn mean_squared_error for documentation on how to control axis.

answered Apr 3, 2016 at 16:17

![]()

Even more numpy

np.square(np.subtract(A, B)).mean()

answered Nov 19, 2017 at 8:11

![]()

Mark SwardstromMark Swardstrom

17.2k6 gold badges62 silver badges70 bronze badges

1

Just for kicks

mse = (np.linalg.norm(A-B)**2)/len(A)

![]()

desertnaut

57.7k27 gold badges140 silver badges167 bronze badges

answered Jun 16, 2020 at 6:26

![]()

Another alternative to the accepted answer that avoids any issues with matrix multiplication:

def MSE(Y, YH):

return np.square(Y - YH).mean()

From the documents for np.square:

Return the element-wise square of the input.

![]()

desertnaut

57.7k27 gold badges140 silver badges167 bronze badges

answered Aug 31, 2017 at 16:04

The standard numpy methods for calculation mean squared error (variance) and its square root (standard deviation) are numpy.var() and numpy.std(), see here and here. They apply to matrices and have the same syntax as numpy.mean().

I suppose that the question and the preceding answers might have been posted before these functions became available.

Remarks on statistics

To answer the comment made by @Drew :

This answer is equivalent to the top answers in this thread. Technically, MSE differs from variance in that it uses «true» value of the parameter, rather than its estimate, see

What’s the difference between the variance and the mean squared error? and What is the Difference between Variance and MSE?. The two quantities then differ by the bias of our estimate of the central parameter. However, when calculating sample variance, as is done in the OP, we cannot really know the value of this parameter. I believe the OP uses term MSE in a loose sense.

Furthermore, the numpy functions proposed above allow for parameter ddof (the number of degrees of freedom), which allows to obtain unbiased variance estimates (contrary to what is claimed in some superficial comparisons between python and R.)

answered Oct 12, 2020 at 9:58

![]()

Roger VadimRoger Vadim

3732 silver badges12 bronze badges

1

What about this to keep with the np.operation style?

mse = np.mean(np.square(A - B))

Just keep in mind that np.mean() with no axis keyword argument specified will output a scalar, just like np.sum().

answered Mar 1 at 6:37

![]()

Время на прочтение

4 мин

Количество просмотров 5.6K

Функции потерь Python являются важной частью моделей машинного обучения. Эти функции показывают, насколько сильно предсказанный моделью результат отличается от фактического.

Существует несколько способов вычислить эту разницу. В этом материале мы рассмотрим некоторые из наиболее распространенных функций потерь.

Ниже будут рассмотрены следующие четыре функции потерь.

-

Среднеквадратическая ошибка

-

Среднеквадратическая ошибка

-

Средняя абсолютная ошибка

-

Кросс-энтропийные потери

Из этих четырех функций потерь первые три применяются к модели классификации.

1. Среднеквадратическая ошибка (MSE)

Среднеквадратичная ошибка (MSE) рассчитывается как среднее значение квадратов разностей между прогнозируемыми и фактически наблюдаемыми значениями. Математически это можно выразить следующим образом:

Реализация MSE на языке Python выглядит следующим образом:

import numpy as np # импортируем библиотеку numpy

def mean_squared_error(act, pred): # функция

diff = pred - act # находим разницу между прогнозируемыми и наблюдаемыми значениями

differences_squared = diff ** 2 # возводим в квадрат (чтобы избавиться от отрицательных значений)

mean_diff = differences_squared.mean() # находим среднее значение

return mean_diff

act = np.array([1.1,2,1.7]) # создаем список актуальных значений

pred = np.array([1,1.7,1.5]) # список прогнозируемых значений

print(mean_squared_error(act,pred))

Выход :

0.04666666666666667Вы также можете использовать mean_squared_error из sklearn для расчета MSE. Вот как работает функция:

from sklearn.metrics import mean_squared_error

act = np.array([1.1,2,1.7])

pred = np.array([1,1.7,1.5])

mean_squared_error(act, pred)

Выход :

0.04666666666666667

2. Корень среднеквадратической ошибки (RMSE)

Итак, ранее, для того, чтобы найти действительную ошибку среди между прогнозируемыми и фактически наблюдаемыми значениями (там могли быть положительные и отрицательные значения), мы возводили их в квадрат (для того чтобы отрицательные значения участвовали в расчетах в полной мере). Это была среднеквадратичная ошибка (MSE).

Корень среднеквадратической ошибки (RMSE) мы используем для того чтобы избавиться от квадратной степени, в которую мы ранее возвели действительную ошибку среди между прогнозируемыми и фактически наблюдаемыми значениями. Математически мы можем представить это следующим образом:

Реализация Python для RMSE выглядит следующим образом:

import numpy as np

def root_mean_squared_error(act, pred):

diff = pred - act # находим разницу между прогнозируемыми и наблюдаемыми значениями

differences_squared = diff ** 2 # возводим в квадрат

mean_diff = differences_squared.mean() # находим среднее значение

rmse_val = np.sqrt(mean_diff) # извлекаем квадратный корень

return rmse_val

act = np.array([1.1,2,1.7])

pred = np.array([1,1.7,1.5])

print(root_mean_squared_error(act,pred))

Выход :

0.21602468994692867

Вы также можете использовать mean_squared_error из sklearn для расчета RMSE. Давайте посмотрим, как реализовать RMSE, используя ту же функцию:

from sklearn.metrics import mean_squared_error

act = np.array([1.1,2,1.7])

pred = np.array([1,1.7,1.5])

mean_squared_error(act, pred, squared = False) #Если установлено значение False, функция возвращает значение RMSE.

Выход :

0.21602468994692867

Если для параметра squared установлено значение True, функция возвращает значение MSE. Если установлено значение False, функция возвращает значение RMSE.

3. Средняя абсолютная ошибка (MAE)

Средняя абсолютная ошибка (MAE) рассчитывается как среднее значение абсолютной разницы между прогнозами и фактическими наблюдениями. Математически мы можем представить это следующим образом:

Реализация Python для MAE выглядит следующим образом:

import numpy as np

def mean_absolute_error(act, pred): #

diff = pred - act # находим разницу между прогнозируемыми и наблюдаемыми значениями

abs_diff = np.absolute(diff) # находим абсолютную разность между прогнозами и фактическими наблюдениями.

mean_diff = abs_diff.mean() # находим среднее значение

return mean_diff

act = np.array([1.1,2,1.7])

pred = np.array([1,1.7,1.5])

mean_absolute_error(act,pred)

Выход :

0.20000000000000004

Вы также можете использовать mean_absolute_error из sklearn для расчета MAE.

from sklearn.metrics import mean_absolute_error

act = np.array([1.1,2,1.7])

pred = np.array([1,1.7,1.5])

mean_absolute_error(act, pred)

Выход :

0.20000000000000004

4. Функция потерь перекрестной энтропии в Python

Функция потерь перекрестной энтропии также известна как отрицательная логарифмическая вероятность. Это чаще всего используется для задач классификации. Проблема классификации — это проблема, в которой вы классифицируете пример как принадлежащий к одному из более чем двух классов.

Давайте посмотрим, как вычислить ошибку в случае проблемы бинарной классификации.

Давайте рассмотрим проблему классификации, когда модель пытается провести классификацию между собакой и кошкой.

Код Python для поиска ошибки приведен ниже.

from sklearn.metrics import log_loss

log_loss(["Dog", "Cat", "Cat", "Dog"],[[.1, .9], [.9, .1], [.8, .2], [.35, .65]])

Выход :

0.21616187468057912

Мы используем метод log_loss из sklearn.

Первый аргумент в вызове функции — это список правильных меток классов для каждого входа. Второй аргумент — это список вероятностей, предсказанных моделью.

Вероятности представлены в следующем формате:

[P(dog), P(cat)]

Заключение

Это руководство было посвящено функциям потерь в Python. Мы рассмотрели различные функции потерь как для задач регрессии, так и для задач классификации. Надеюсь, вам понравился материал, ведь все было достаточно легко и понятно!

Кстати, для тех, кто хотел бы пойти дальше в изучении функций потерь, мы предлагаем разобрать одну вот такую — это очень интересная функция потерь Triplet Loss в Python (функцию тройных потерь), которую для вас любезно подготовил автор.

The mean squared error is a common way to measure the prediction accuracy of a model. In this tutorial, you’ll learn how to calculate the mean squared error in Python. You’ll start off by learning what the mean squared error represents. Then you’ll learn how to do this using Scikit-Learn (sklean), Numpy, as well as from scratch.

Table of Contents

What is the Mean Squared Error

The mean squared error measures the average of the squares of the errors. What this means, is that it returns the average of the sums of the square of each difference between the estimated value and the true value.

The MSE is always positive, though it can be 0 if the predictions are completely accurate. It incorporates the variance of the estimator (how widely spread the estimates are) and its bias (how different the estimated values are from their true values).

The formula looks like below:

Now that you have an understanding of how to calculate the MSE, let’s take a look at how it can be calculated using Python.

Interpreting the Mean Squared Error

The mean squared error is always 0 or positive. When a MSE is larger, this is an indication that the linear regression model doesn’t accurately predict the model.

An important piece to note is that the MSE is sensitive to outliers. This is because it calculates the average of every data point’s error. Because of this, a larger error on outliers will amplify the MSE.

There is no “target” value for the MSE. The MSE can, however, be a good indicator of how well a model fits your data. It can also give you an indicator of choosing one model over another.

Loading a Sample Pandas DataFrame

Let’s start off by loading a sample Pandas DataFrame. If you want to follow along with this tutorial line-by-line, simply copy the code below and paste it into your favorite code editor.

# Importing a sample Pandas DataFrame

import pandas as pd

df = pd.DataFrame.from_dict({

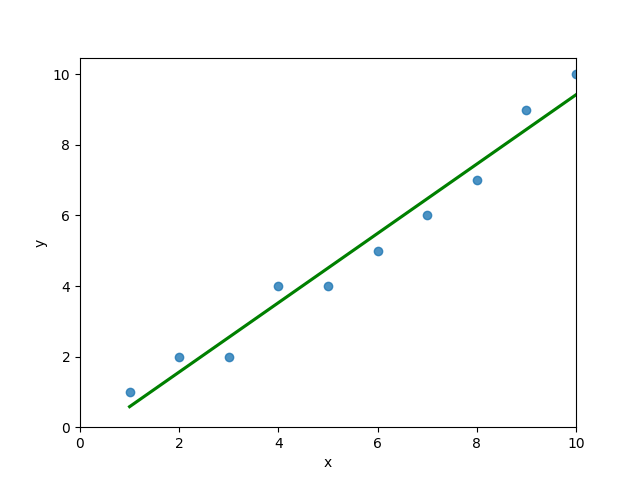

'x': [1,2,3,4,5,6,7,8,9,10],

'y': [1,2,2,4,4,5,6,7,9,10]})

print(df.head())

# x y

# 0 1 1

# 1 2 2

# 2 3 2

# 3 4 4

# 4 5 4You can see that the editor has loaded a DataFrame containing values for variables x and y. We can plot this data out, including the line of best fit using Seaborn’s .regplot() function:

# Plotting a line of best fit

import seaborn as sns

import matplotlib.pyplot as plt

sns.regplot(data=df, x='x', y='y', ci=None)

plt.ylim(bottom=0)

plt.xlim(left=0)

plt.show()This returns the following visualization:

The mean squared error calculates the average of the sum of the squared differences between a data point and the line of best fit. By virtue of this, the lower a mean sqared error, the more better the line represents the relationship.

We can calculate this line of best using Scikit-Learn. You can learn about this in this in-depth tutorial on linear regression in sklearn. The code below predicts values for each x value using the linear model:

# Calculating prediction y values in sklearn

from sklearn.linear_model import LinearRegression

model = LinearRegression()

model.fit(df[['x']], df['y'])

y_2 = model.predict(df[['x']])

df['y_predicted'] = y_2

print(df.head())

# Returns:

# x y y_predicted

# 0 1 1 0.581818

# 1 2 2 1.563636

# 2 3 2 2.545455

# 3 4 4 3.527273

# 4 5 4 4.509091Calculating the Mean Squared Error with Scikit-Learn

The simplest way to calculate a mean squared error is to use Scikit-Learn (sklearn). The metrics module comes with a function, mean_squared_error() which allows you to pass in true and predicted values.

Let’s see how to calculate the MSE with sklearn:

# Calculating the MSE with sklearn

from sklearn.metrics import mean_squared_error

mse = mean_squared_error(df['y'], df['y_predicted'])

print(mse)

# Returns: 0.24727272727272714This approach works very well when you’re already importing Scikit-Learn. That said, the function works easily on a Pandas DataFrame, as shown above.

In the next section, you’ll learn how to calculate the MSE with Numpy using a custom function.

Calculating the Mean Squared Error from Scratch using Numpy

Numpy itself doesn’t come with a function to calculate the mean squared error, but you can easily define a custom function to do this. We can make use of the subtract() function to subtract arrays element-wise.

# Definiting a custom function to calculate the MSE

import numpy as np

def mse(actual, predicted):

actual = np.array(actual)

predicted = np.array(predicted)

differences = np.subtract(actual, predicted)

squared_differences = np.square(differences)

return squared_differences.mean()

print(mse(df['y'], df['y_predicted']))

# Returns: 0.24727272727272714The code above is a bit verbose, but it shows how the function operates. We can cut down the code significantly, as shown below:

# A shorter version of the code above

import numpy as np

def mse(actual, predicted):

return np.square(np.subtract(np.array(actual), np.array(predicted))).mean()

print(mse(df['y'], df['y_predicted']))

# Returns: 0.24727272727272714Conclusion

In this tutorial, you learned what the mean squared error is and how it can be calculated using Python. First, you learned how to use Scikit-Learn’s mean_squared_error() function and then you built a custom function using Numpy.

The MSE is an important metric to use in evaluating the performance of your machine learning models. While Scikit-Learn abstracts the way in which the metric is calculated, understanding how it can be implemented from scratch can be a helpful tool.

Additional Resources

To learn more about related topics, check out the tutorials below:

- Pandas Variance: Calculating Variance of a Pandas Dataframe Column

- Calculate the Pearson Correlation Coefficient in Python

- How to Calculate a Z-Score in Python (4 Ways)

- Official Documentation from Scikit-Learn

Mean squared error (MSE) of an estimator measures the average of the squared errors, it means averages squared difference between the actual and estimated value.

MSE is almost positive because MSE of an estimator does not account for information that could produce more accurate estimate.

In statistical modelling, MSE is defined as the difference between actual values and predicted values by the model and used to determine prediction accuracy of a model.

In this tutorial, we will discuss about how to calculate mean squared error (MSE) in python.

Mean Squared Error Formula

The mean squared error (MSE) formula is defined as follows:

Where,

n = sample data points

y – actual sizey^ – predictive values

MSE is the means of squares of the errors ( yi – yi^)2.

We will be using numpy library to generate actual and predication values.

As there is no in built function available in python to calculate mean squared error (MSE), we will write simple function for calculation as per mean squared error formula.

pip install numpy

If you don’t have numpy package installed on your system, use below command in command prompt

pip install numpy

Lets understand with examples about how to calculate mean squared error (MSE) in python with given below python code

import numpy as np

def mse(actual,prediction):

return np.square(np.subtract(actual,prediction)).mean()

#define Actual and Prediction data array

actual = np.array([10,11,12,12,14,18,20])

pred = np.array([9,10,13,14,17,16,18])

#Calculate MSE

result = mse(actual,pred)

#print the result

print("Mean squared error (MSE) :", result)

In the above example, we have created actual and prediction array with the help of numpy package array function.

We have written simple function mse() as per mean squared error formula which takes two parameters actual and prediction data array. It calculates mean of the squares of (actual – prediction) using numpy packages square and mean function.

Above code returns mean squared error (MSE) value for given actual and prediction model is 3.42857

Lets check out Mean squared Error (MSE) calculation with few other examples

Info Tip: How to calculate SMAPE in Python!

Example 1 – Mean Squared Error Calculation

Lets assume we have actual and forecast dataset as below

actual = [4,7,3,9,12,8,14,10,12,12]

prediction = [5,7,3,8,10,8,12,11,11,13]

Calculate MSE for given model.

Here, again we will be using numpy package to create actual and prediction array and simple mse() function for mean squared error calculation in python code as below

import numpy as np

def mse(actual,pred):

return np.square(np.subtract(actual,pred)).mean()

#define Actual and Prediction data array

actual = np.array([4,7,3,9,12,8,14,10,12,12])

pred = np.array([5,7,3,8,10,8,12,11,11,13])

#Calculate MSE

result = mse(actual,pred)

#print the result

print("Mean squared error (MSE) :", result)

Above code returns mean squared error (MSE) for given actual and prediction dataset is 1.3

Info Tip: How to calculate rolling correlation in Python!

Example 2 – Mean Squared Error Calculation

Lets take another example with below actual and prediction data values

actual = [-2,-1,1,4]

prediction = [-3,-1,2,3]

Calcualte MSE for above model.

Using below python code, lets calculate MSE

import numpy as np

def mse(actual,pred):

return np.square(np.subtract(actual,pred)).mean()

#define Actual and Prediction data array

actual = np.array([-2,-1,1,4])

pred = np.array([-3,-1,2,3])

#Calculate MSE

result = mse(actual,pred)

#print the result

print("Mean squared error (MSE) :", result)

Above code returns mean squared error (MSE) for given actual and prediction dataset is 0.75. It means it has less squared error and hence this model predicts more accuracy.

Info Tip: How to calculate z score in Python!

Conclusion

I hope, you may find how to calculate MSE in python tutorial with step by step illustration of examples educational and helpful.

Mean squared error (MSE) measures the prediction accuracy of model. Minimizing MSE is key criterion in selecting estimators.