Эту функцию называют также «логлосс» (logloss / log_loss), перекрёстной / кросс-энтропией (Cross Entropy) и часто используют в задачах классификации. Разберёмся, почему её используют и какой смысл она имеет. Для чтения поста нужна неплохая ML-математическая подготовка, но даже новичкам я бы рекомендовал почитать (хотя я не очень заботился, чтобы «всё объяснялось на пальцах»).

Начнём издалека…

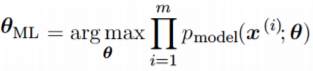

Вспомним, как решается задача линейной регрессии. Итак, мы хотим получить линейную функцию (т.е. веса w), которая приближает целевое значение с точностью до ошибки:

Здесь мы предположили, что ошибка нормально распределена, x – признаковое описание объекта (возможно, в нём есть и фиктивный константный признак, чтобы в линейной функции был свободный член). Тогда мы знаем как распределены ответы нашей функции и можем записать функцию правдоподобия выборки (т.е. произведение плотностей, в которые подставлены значения из обучающей выборки) и воспользоваться методом максимального правдоподобия (в котором для определения значений параметров берётся максимум правдоподобия, а чаще – его логарифма):

В итоге оказывается, что максимизация правдоподобия эквивалентна минимизации среднеквадратичной ошибки (MSE), т.е. эта функция ошибки не зря широко используется в задачах регрессии. Кроме того, что она вполне логична, легко дифференцируема по параметрам и легко минимизируется, она ещё и теоретически обосновывается с помощью метода максимального правдоподобия в случае, если линейная модель соответствует данным с точностью до нормального шума.

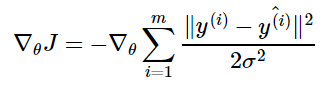

Давайте ещё посмотрим, как реализуется метод стохастического градиента (SGD) для минимизации MSE: надо взять производную функции ошибки для конкретного объекта и записать формулу коррекции весов в виде «шага в сторону антиградиента»:

Получили, что веса линейной модели при её обучении методом SGD корректируются с помощью добавки вектора признаков. Коэффициент, с которым добавляют, зависит от «агрессивности алгоритма» (параметр альфа, который называют темпом обучения) и разности «ответ алгоритма – правильный ответ». Кстати, если разница нулевая (т.е. на данном объекте алгоритм выдаёт точный ответ), то коррекция весов не производится.

Log Loss

Теперь давайте, наконец, поговорим о «логлоссе». Рассматриваем задачу классификации с двумя классами: 0 и 1. Обучающую выборку можно рассматривать, как реализацию обобщённой схемы Бернулли: для каждого объекта генерируется случайная величина, которая с вероятностью p (своей для каждого объекта) принимает значение 1 и с вероятностью (1–p) – 0. Предположим, что мы как раз и строим нашу модель так, чтобы она генерировала правильные вероятности, но тогда можно записать функцию правдоподобия:

После логарифмирования правдоподобия получили, что его максимизация эквивалентна минимизации последнего записанного выражения. Именно его и называют «логистической функции ошибки». Для задачи бинарной классификации, в которой алгоритм должен выдать вероятность принадлежности классу 1, она логична ровно настолько, насколько логична MSE в задаче линейной регрессии с нормальным шумом (поскольку обе функции ошибки выводятся из метода максимального правдоподобия).

Часто гораздо более понятна такая запись logloss-ошибки на одном объекте:

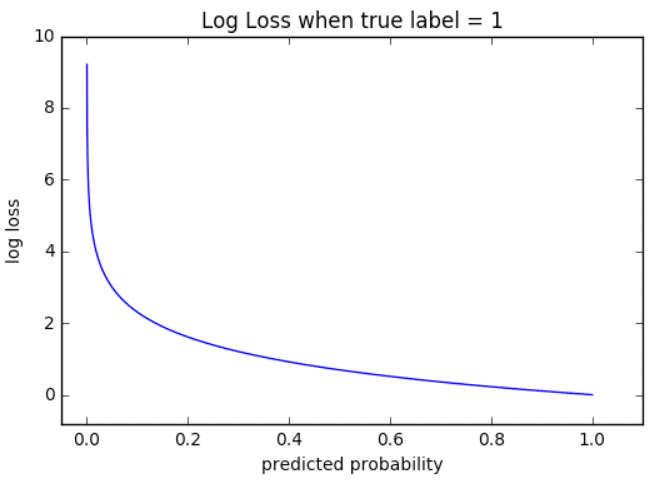

Отметим неприятное свойство логосса: если для объекта 1го класса мы предсказываем нулевую вероятность принадлежности к этому классу или, наоборот, для объекта 0го – единичную вероятность принадлежности к классу 1, то ошибка равна бесконечности! Таким образом, грубая ошибка на одном объекте сразу делает алгоритм бесполезным. На практике часто логлосс ограничивают каким-то большим числом (чтобы не связываться с бесконечностями).

Если задаться вопросом, какой константный алгоритм оптимален для выборки из q_1 представителей класса 1 и q_0 представителей класса 0, q_1 + q_0 = q , то получим

Последний ответ получается взятием производной и приравниванием её к нулю. Описанную задачу приходится решать, например, при построении решающих деревьев (какую метку приписывать листу, если в него попали представители разных классов). На рис. 2 изображён график log_loss-ошибки константного алгоритма для выборки из четырёх объектов класса 0 и 6 объектов класса 1.

Представим теперь, что мы знаем, что объект принадлежит к классу 1 вероятностью p, посмотрим, какой ответ оптимален на этом объекте с точки зрения log_loss: матожидание нашей ошибки

Для минимизации ошибки мы опять взяли производную и приравняли к нулю. Мы получили, что оптимально для каждого объекта выдавать его вероятность принадлежности к классу 1! Таким образом, для минимизации log_loss надо уметь вычислять (оценивать) вероятности принадлежности классам!

Если подставить полученное оптимальное решение в минимизируемый функционал, то получим энтропию:

Это объясняет, почему при построении решающих деревьев в задачах классификации (а также случайных лесов и деревьях в бустингах) применяют энтропийный критерий расщепления (ветвления). Дело в том, что оценка принадлежности к классу 1 часто производится с помощью среднего арифметического меток в листе. В любом случае, для конкретного дерева эта вероятность будет одинакова для всех объектов в листе, т.е. константой. Таким образом, энтропия в листе примерно равна логлосс-ошибке константного решения. Используя энтропийный критерий мы неявно оптимизируем логлосс!

В каких пределах может варьироваться logloss? Ясно, что минимальное значение 0, максимальное – +∞, но эффективным максимальным можно считать ошибку при использовании константного алгоритма (вряд же мы в итоге решения задачи придумаем алгоритм хуже константы?!), т.е.

Интересно, что если брать логарифм по основанию 2, то на сбалансированной выборке это отрезок [0, 1].

Связь с логистической регрессией

Слово «логистическая» в названии ошибки намекает на связь с логистической регрессией – это как раз метод для решения задачи бинарной классификации, который получает вероятность принадлежности к классу 1. Но пока мы исходили из общих предположений, что наш алгоритм генерирует эту вероятность (алгоритмом может быть, например, случайный лес или бустинг над деревьями). Покажем, что тесная связь с логистической регрессией всё-таки есть… посмотрим, как настраивается логистическая регрессия (т.е. сигмоида от линейной комбинации) на эту функцию ошибки методом SGD.

Как видим, корректировка весов точно такая же, как и при настройке линейной регрессии! На самом деле, это говорит о родстве разных регрессий: линейной и логистической, а точнее, о родстве распределений: нормального и Бернулли. Желающие могут внимательно почитать лекцию Эндрю Ына.

Во многих книгах логистической функцией ошибки (т.е. именно «logistic loss») называется другое выражение, которое мы сейчас получим, подставив выражение для сигмоиды в logloss и сделав переобозначение: считаем, что метки классов теперь –1 и +1, тогда

Полезно посмотреть на график функции, центральной в этом представлении:

Как видно, это сглаженный (всюду дифференцируемый) аналог функции max(0, x), которую в глубоком обучении принято называть ReLu (Rectified Linear Unit). Если при настройке весов минимизировать logloss, то таким образом мы настраиваем классическую логистическую регрессию, если же использовать ReLu, чуть-чуть подправить аргумент и добавить регуляризацию, то получаем классическую настройку SVM:

выражение под знаком суммы принято называть Hinge loss. Как видим, часто с виду совсем разные методы можно получать «немного подправив» оптимизируемые функции на похожие. Между прочим, при обучении RVM (Relevance vector machine) используется тоже очень похожий функционал:

Связь с расхождением Кульбака-Лейблера

Расхождение (дивергенцию) Кульбака-Лейблера (KL, Kullback–Leibler divergence) часто используют (особенно в машинном обучении, байесовском подходе и теории информации) для вычисления непохожести двух распределений. Оно определяется по следующей формуле:

где P и Q – распределения (первое обычно «истинное», а второе – то, про которое нам интересно, насколько оно похоже на истинное), p и q – плотности этих распределений. Часто KL-расхождение называют расстоянием, хотя оно не является симметричным и не удовлетворяет неравенству треугольника. Для дискретных распределений формулу записывают так:

P_i, Q_i – вероятности дискретных событий. Давайте рассмотрим конкретный объект x с меткой y. Если алгоритм выдаёт вероятность принадлежности первому классу – a, то предполагаемое распределение на событиях «класс 0», «класс 1» – (1–a, a), а истинное – (1–y, y), поэтому расхождение Кульбака-Лейблера между ними

что в точности совпадает с logloss.

Настройка на logloss

Один из методов «подгонки» ответов алгоритма под logloss – калибровка Платта (Platt calibration). Идея очень простая. Пусть алгоритм порождает некоторые оценки принадлежности к 1му классу – a. Метод изначально разрабатывался для калибровки ответов алгоритма опорных векторов (SVM), этот алгоритм в простейшей реализации разделяет объекты гиперплоскостью и просто выдаёт номер класса 0 или 1, в зависимости от того, с какой стороны гиперплоскости объект расположен. Но если мы построили гиперплоскость, то для любого объекта можем вычислить расстояние до неё (со знаком минус, если объект лежит в полуплоскости нулевого класса). Именно эти расстояния со знаком r мы будем превращать в вероятности по следующей формуле:

неизвестные параметры α, β обычно определяются методом максимального правдоподобия на отложенной выборке (calibration set).

Проиллюстрируем применение метода на реальной задаче, которую автор решал недавно. На рис. показаны ответы (в виде вероятностей) двух алгоритмов: градиентного бустинга (lightgbm) и случайного леса (random forest).

Видно, что качество леса намного ниже и он довольно осторожен: занижает вероятности у объектов класса 1 и завышает у объектов класса 0. Упорядочим все объекты по возрастанию вероятностей (RF), разобьем на k равных частей и для каждой части вычислим среднее всех ответов алгоритма и среднее всех правильных ответов. Результат показан на рис. 5 – точки изображены как раз в этих двух координатах.

Нетрудно видеть, что точки располагаются на линии, похожей на сигмоиду – можно оценить параметр сжатия-растяжения в ней, см. рис. 6. Оптимальная сигмоида показана розовым цветом на рис. 5. Если подвергать ответы такой сигмоидной деформации, то логлосс-ошибка случайного леса снижается с 0.37 до 0.33.

Обратите внимание, что здесь мы деформировали ответы случайного леса (это были оценки вероятности – и все они лежали на отрезке [0, 1]), но из рис. 5 видно, что для деформации нужна именно сигмоида. Практика показывает, что в 80% ситуаций для улучшения logloss-ошибки надо деформировать ответы именно с помощью сигмоиды (для меня это также часть объяснения, почему именно такие функции успешно используются в качестве функций активаций в нейронных сетях).

Ещё один вариант калибровки – монотонная регрессия (Isotonic regression).

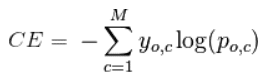

Многоклассовый logloss

Для полноты картины отметим, что logloss обобщается и на случай нескольких классов естественным образом:

здесь q – число элементов в выборке, l – число классов, a_ij – ответ (вероятность) алгоритма на i-м объекте на вопрос принадлежности его к j-му классу, y_ij=1 если i-й объект принадлежит j-му классу, в противном случае y_ij=0.

На посошок…

В каждом подобном посте я стараюсь написать что-то из мира машинного обучения, что, с одной стороны, просто и понятно, а с другой – изложение этого не встречается больше нигде. Например, есть такой естественный вопрос: почему в задачах классификации при построении решающих деревьев используют энтропийный критерий расщепления? Во всех курсах его (критерий) преподносят либо как эвристику, которую «вполне естественно использовать», либо говорят, что «энтропия похожа на кросс-энтропию». Сейчас стоимость некоторых курсов по машинному обучению достигает нескольких сотен тысяч рублей, но «профессиональные инструкторы» не могут донести простую цепочку:

- в статистической теории обучения настройка алгоритма производится максимизацией правдоподобия,

- в задаче бинарной классификации это эквивалентно минимизации логлосса, а сам минимум как раз равен энтропии,

- поэтому использование энтропийного критерия фактически эквивалентно выбору расщепления, минимизирующего логлосс.

Если Вы всё-таки отдали несколько сотен тысяч рублей, то можете проверить «профессиональность инструктора» следующими вопросами:

- Энтропия в листе примерно равна logloss-ошибке константного решения. Почему не использовать саму ошибку, а не приближённое значение? Или, как часто происходит в задачах оптимизации, её верхнюю оценку?

- Минимизации какой ошибки соответствует критерий расщепления Джини?

- Можно показать, что если в задаче бинарной классификации использовать в качестве функции ошибки среднеквадратичное отклонение, то также, как и для логлосса, оптимальным ответом на объекте будет вероятность его принадлежности к классу 1. Почему тогда не использовать такую функцию ошибки?

Ответы типа «так принято», «такой функции не существует», «это только для регрессии», естественно, заведомо неправильные. Если Вам не ответят с такой же степенью подробности, как в этом посте, то Вы точно переплатили;)

П.С. Что ещё почитать…

В этом блоге я публиковал уже несколько постов по метрикам качества…

- AUC ROC (площадь под кривой ошибок)

- Задачки про AUC (ROC)

- Знакомьтесь, Джини

И буквально на днях вышла классная статья Дмитрия Петухова про коэффициент Джини, читать обязательно:

- Коэффициент Джини. Из экономики в машинное обучение

В этой статье, мы будем разбирать теоретические выкладки преобразования функции линейной регрессии в функцию обратного логит-преобразования (иначе говорят, функцию логистического отклика). Затем, воспользовавшись арсеналом метода максимального правдоподобия, в соответствии с моделью логистической регрессии, выведем функцию потерь Logistic Loss, или другими словами, мы определим функцию, с помощью которой в модели логистической регрессии подбираются параметры вектора весов  .

.

План статьи:

- Повторим о прямолинейной зависимости между двумя переменными

- Выявим необходимость преобразования функции линейной регрессии

в функцию логистического отклика

в функцию логистического отклика - Проведем преобразования и выведем функцию логистического отклика

- Попытаемся понять, чем плох метод наименьших квадратов при подборе параметров функции Logistic Loss

- Используем метод максимального правдоподобия для определения функции подбора параметров :

5.1. Случай 1: функция Logistic Loss для объектов с обозначением классов 0 и 1:

5.2. Случай 2: функция Logistic Loss для объектов с обозначением классов -1 и +1:

в функцию логистического отклика

в функцию логистического отклика

Статья изобилует простыми примерами, в которых все расчеты легко произвести устно или на бумаге, в некоторых случаях может потребоваться калькулятор. Так что подготовьтесь

Данная статья в большей мере рассчитана на датасайнтистов с начальным уровнем познаний в основах машинного обучения.

В статье также будет приведен код для отрисовки графиков и расчетов. Весь код написан на языке python 2.7. Заранее поясню о «новизне» используемой версии — таково одно из условий прохождения известного курса от Яндекса на не менее известной интернет-площадке онлайн образования Coursera, и, как можно предположить, материал подготовлен по мотивам этого курса.

01. Прямолинейная зависимость

Вполне резонно задать вопрос — причем здесь прямолинейная зависимость и логистическая регрессия?

Все просто! Логистическая регрессия представляет собой одну из моделей, которые относятся к линейному классификатору. Простыми словами, задачей линейного классификатора является предсказание целевых значений  от переменных (регрессоров)

от переменных (регрессоров)  . При этом считается, что зависимость между признаками и целевыми значениями линейная. Отсюда собственно и название классификатора — линейный. Если очень грубо обобщить, то в основе модели логистической регрессии лежит предположение о наличии линейной зависимости между признаками и целевыми значениями . Вот она — связь.

. При этом считается, что зависимость между признаками и целевыми значениями линейная. Отсюда собственно и название классификатора — линейный. Если очень грубо обобщить, то в основе модели логистической регрессии лежит предположение о наличии линейной зависимости между признаками и целевыми значениями . Вот она — связь.

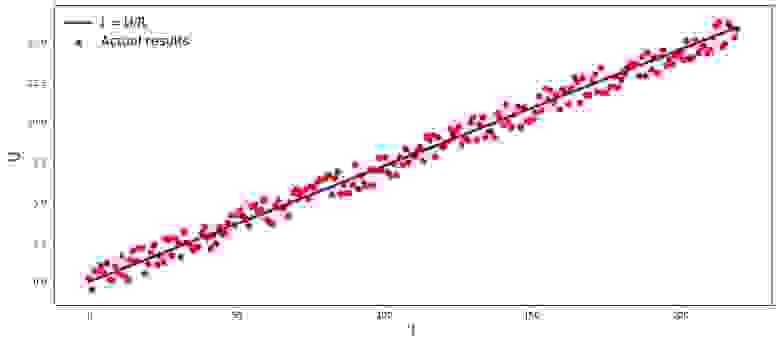

В студии первый пример, и он, правильно, о прямолинейной зависимости исследуемых величин. В процессе подготовки статьи наткнулся на пример, набивший уже многим оскомину — зависимость силы тока от напряжения («Прикладной регрессионный анализ», Н.Дрейпер, Г.Смит). Здесь мы его тоже рассмотрим.

В соответствии с законом Ома:

, где

, где  — сила тока,

— сила тока,  — напряжение,

— напряжение,  — сопротивление.

— сопротивление.

Если бы мы не знали закон Ома, то могли бы найти зависимость эмпирически, изменяя и измеряя , поддерживая при этом фиксированным. Тогда мы бы увидели, что график зависимости от дает более или менее прямую линию, проходящую через начало координат. Мы сказали «более или менее», так как, хотя зависимость фактически точная, наши измерения могут содержать малые ошибки, и поэтому точки на графике, возможно не попадут строго на линию, а будут разбросаны вокруг нее случайным образом.

График 1 «Зависимость от »

Код отрисовки графика

import matplotlib.pyplot as plt

%matplotlib inline

import numpy as np

import random

R = 13.75

x_line = np.arange(0,220,1)

y_line = []

for i in x_line:

y_line.append(i/R)

y_dot = []

for i in y_line:

y_dot.append(i+random.uniform(-0.9,0.9))

fig, axes = plt.subplots(figsize = (14,6), dpi = 80)

plt.plot(x_line,y_line,color = 'purple',lw = 3, label = 'I = U/R')

plt.scatter(x_line,y_dot,color = 'red', label = 'Actual results')

plt.xlabel('I', size = 16)

plt.ylabel('U', size = 16)

plt.legend(prop = {'size': 14})

plt.show()

02. Необходимость преобразований уравнения линейной регрессии

Рассмотрим очередной пример. Представим, что мы работаем в банке и перед нами задача определить вероятность возврата кредита заемщиком в зависимости от некоторых факторов. Для упрощения задачи, рассмотрим только два фактора: месячная зарплата заемщика и месячный размер платежа на погашение кредита.

Задача очень условная, но на этом примере мы сможем понять, почему для ее решения недостаточно применения функции линейной регрессии, а также узнаем какие преобразования с функцией требуется провести.

Возвращаемся к примеру. Понятно, что чем выше зарплата, тем больше заемщик сможет ежемесячно направлять на погашение кредита. При этом, для определенного диапазона зарплат эта зависимость будет вполне себе линейная. Например, возьмем диапазон зарплат от 60.000Р до 200.000Р и предположим, что в указанном диапазоне заработных плат, зависимость размера ежемесячного платежа от размера заработной платы — линейная. Допустим, для указанного диапазона размера заработных плат было выявлено, что соотношение зарплаты к платежу не может опускаться ниже 3 и еще у заемщика должно оставаться в запасе 5.000Р. И только в таком случае, мы будем считать, что заемщик вернет кредит банку. Тогда, уравнение линейной регрессии примет вид:

где  ,

,  ,

,  ,

,  — зарплата

— зарплата  -го заемщика,

-го заемщика,  — платеж по кредиту -го заемщика.

— платеж по кредиту -го заемщика.

Подставляя в уравнение зарплату и платеж по кредиту с фиксированными параметрами можно принять решение о выдаче или отказе кредита.

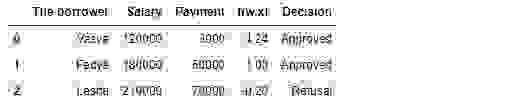

Забегая вперед, отметим, что, при заданных параметрах функция линейной регрессии, применяемая в функции логистичиеского отклика будет выдавать большие значения, которые затруднят проведение расчетов по определению вероятностей погашения кредита. Поэтому, предлагается уменьшить наши коэффициенты, скажем так, в 25.000 раз. От этого преобразования в коэффициентах, решение о выдачи кредита не изменится. Запомним этот момент на будущее, а сейчас чтобы было еще понятнее, о чем речь, рассмотрим ситуация с тремя потенциальными заемщиками.

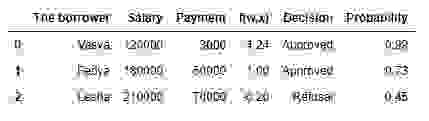

Таблица 1 «Потенциальные заемщики»

Код для формирования таблицы

import pandas as pd

r = 25000.0

w_0 = -5000.0/r

w_1 = 1.0/r

w_2 = -3.0/r

data = {'The borrower':np.array(['Vasya', 'Fedya', 'Lesha']),

'Salary':np.array([120000,180000,210000]),

'Payment':np.array([3000,50000,70000])}

df = pd.DataFrame(data)

df['f(w,x)'] = w_0 + df['Salary']*w_1 + df['Payment']*w_2

decision = []

for i in df['f(w,x)']:

if i > 0:

dec = 'Approved'

decision.append(dec)

else:

dec = 'Refusal'

decision.append(dec)

df['Decision'] = decision

df[['The borrower', 'Salary', 'Payment', 'f(w,x)', 'Decision']]

В соответствии с данными таблицы, Вася при зарплате в 120.000Р хочет получить такой кредит, чтобы ежемесячного гасить его по 3.000Р. Нами было определено, что для одобрения кредита, размер заработной платы Васи должен превышать в три раза размер платежа, и чтобы еще оставалось 5.000Р. Этому требованию Вася удовлетворяет:  . Остается даже 106.000Р. Несмотря на то, что при расчете

. Остается даже 106.000Р. Несмотря на то, что при расчете  мы уменьшили коэффициенты в 25.000 раз, результат получили тот же — кредит может быть одобрен. Федя тоже получит кредит, а вот Леше, несмотря на то, что он получает больше всех, придется поумерить свои аппетиты.

мы уменьшили коэффициенты в 25.000 раз, результат получили тот же — кредит может быть одобрен. Федя тоже получит кредит, а вот Леше, несмотря на то, что он получает больше всех, придется поумерить свои аппетиты.

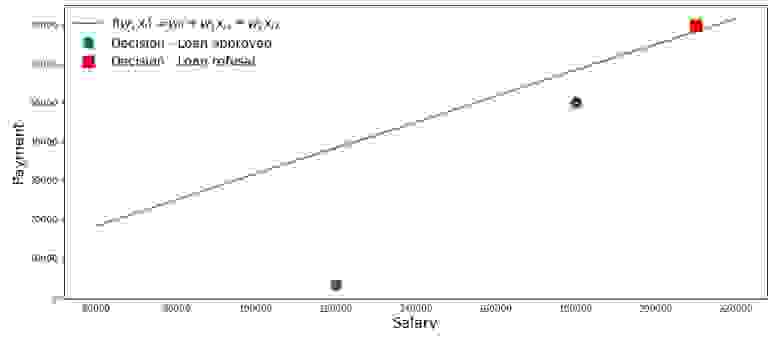

Нарисуем график по такому случаю.

График 2 «Классификация заемщиков»

Код для отрисовки графика

salary = np.arange(60000,240000,20000)

payment = (-w_0-w_1*salary)/w_2

fig, axes = plt.subplots(figsize = (14,6), dpi = 80)

plt.plot(salary, payment, color = 'grey', lw = 2, label = '$f(w,x_i)=w_0 + w_1x_{i1} + w_2x_{i2}$')

plt.plot(df[df['Decision'] == 'Approved']['Salary'], df[df['Decision'] == 'Approved']['Payment'],

'o', color ='green', markersize = 12, label = 'Decision - Loan approved')

plt.plot(df[df['Decision'] == 'Refusal']['Salary'], df[df['Decision'] == 'Refusal']['Payment'],

's', color = 'red', markersize = 12, label = 'Decision - Loan refusal')

plt.xlabel('Salary', size = 16)

plt.ylabel('Payment', size = 16)

plt.legend(prop = {'size': 14})

plt.show()

Итак, наша прямая, построенная в соответствии с функцией  , отделяет «плохих» заемщиков от «хороших». Те заемщики, у кого желания не совпадают с возможностями находятся выше прямой (Леша), те же, кто способен согласно параметрам нашей модели, вернуть кредит, находятся под прямой (Вася и Федя). Иначе можно сказать так — наша прямая разделяет заемщиков на два класса. Обозначим их следующим образом: к классу

, отделяет «плохих» заемщиков от «хороших». Те заемщики, у кого желания не совпадают с возможностями находятся выше прямой (Леша), те же, кто способен согласно параметрам нашей модели, вернуть кредит, находятся под прямой (Вася и Федя). Иначе можно сказать так — наша прямая разделяет заемщиков на два класса. Обозначим их следующим образом: к классу  отнесем тех заемщиков, которые скорее всего вернут кредит, к классу

отнесем тех заемщиков, которые скорее всего вернут кредит, к классу  или

или  отнесем тех заемщиков, которые скорее всего не смогут вернуть кредит.

отнесем тех заемщиков, которые скорее всего не смогут вернуть кредит.

Обобщим выводы из этого простенького примера. Возьмем точку  и, подставляя координаты точки в соответствующее уравнение прямой , рассмотрим три варианта:

и, подставляя координаты точки в соответствующее уравнение прямой , рассмотрим три варианта:

- Если точка находится под прямой, и мы относим ее к классу , то значение функции будет положительным от до . Значит мы можем считать, что вероятность погашения кредита, находится в пределах . Чем больше значение функции, тем выше вероятность.

- Если точка находится над прямой и мы относим ее к классу или , то значение функции будет отрицательным от до . Тогда мы будем считать, что вероятность погашения задолженности находится в пределах и, чем больше по модулю значение функции, тем выше наша уверенность.

- Точка находится на прямой, на границе между двумя классами. В таком случае значение функции будет равно и вероятность погашения кредита равна .

![$(0.5,1]$](https://habrastorage.org/getpro/habr/formulas/e52/d01/8f8/e52d018f87e1844bc2e714af79f0cdf0.svg) . Чем больше значение функции, тем выше вероятность.

. Чем больше значение функции, тем выше вероятность. и, чем больше по модулю значение функции, тем выше наша уверенность.

и, чем больше по модулю значение функции, тем выше наша уверенность. .

.

Теперь, представим, что у нас не два фактора, а десятки, заемщиков не три, а тысячи. Тогда вместо прямой у нас будет m-мерная плоскость и коэффициенты  у нас будут взяты не с потолка, а выведены по всем правилам, да на основе накопленных данных о заемщиках, вернувших или не вернувших кредит. И действительно, заметьте, мы сейчас отбираем заемщиков при уже известных коэффициентах . На самом же деле, задача модели логистической регрессии как раз и состоит в том, чтобы определить параметры , при которых значение функции потерь Logistic Loss будет стремиться к минимальному. Но о том, как рассчитывается вектор , мы еще узнаем в 5-м разделе статьи. А пока возвращаемся на землю обетованную — к нашему банкиру и трем его клиентам.

у нас будут взяты не с потолка, а выведены по всем правилам, да на основе накопленных данных о заемщиках, вернувших или не вернувших кредит. И действительно, заметьте, мы сейчас отбираем заемщиков при уже известных коэффициентах . На самом же деле, задача модели логистической регрессии как раз и состоит в том, чтобы определить параметры , при которых значение функции потерь Logistic Loss будет стремиться к минимальному. Но о том, как рассчитывается вектор , мы еще узнаем в 5-м разделе статьи. А пока возвращаемся на землю обетованную — к нашему банкиру и трем его клиентам.

Благодаря функции мы знаем кому можно дать кредит, а кому нужно отказать. Но с такой информацией к директору идти нельзя, ведь от нас хотели получить вероятность возврата кредита каждым заемщиком. Что делать? Ответ простой — нам нужно как-то преобразовать функцию , значения которой лежат в диапазоне  на функцию, значения которой будут лежать в диапазоне

на функцию, значения которой будут лежать в диапазоне ![$[0,1]$](https://habrastorage.org/getpro/habr/formulas/a5d/538/f83/a5d538f83bd73f9d1c9e8338db9a398a.svg) . И такая функция существует, ее называют функцией логистического отклика или обратного-логит преобразования. Знакомьтесь:

. И такая функция существует, ее называют функцией логистического отклика или обратного-логит преобразования. Знакомьтесь:

Посмотрим по шагам как получается функция логистического отклика. Отметим, что шагать мы будем в обратную сторону, т.е. мы предположим, что нам известно значение вероятности, которое лежит в пределах от до  и далее мы будем «раскручивать» это значение на всю область чисел от

и далее мы будем «раскручивать» это значение на всю область чисел от  до

до  .

.

03. Выводим функцию логистического отклика

Шаг 1. Переведем значения вероятности в диапазон

На время трансформации функции в функцию логистического отклика  мы оставим в покое нашего кредитного аналитика, а вместо этого пройдемся по букмекерским конторам. Нет, конечно, ставки делать мы не будем, все что нас там интересует, так это смысл выражения, например, шанс 4 к 1. Шансы, знакомые всем делающим ставки игрокам, являются соотношением «успехов» к «неуспехам». С точки зрения вероятностей, шансы — это вероятность наступления события, деленная на вероятность того, что событие не произойдет. Запишем формулу шанса наступления события

мы оставим в покое нашего кредитного аналитика, а вместо этого пройдемся по букмекерским конторам. Нет, конечно, ставки делать мы не будем, все что нас там интересует, так это смысл выражения, например, шанс 4 к 1. Шансы, знакомые всем делающим ставки игрокам, являются соотношением «успехов» к «неуспехам». С точки зрения вероятностей, шансы — это вероятность наступления события, деленная на вероятность того, что событие не произойдет. Запишем формулу шанса наступления события  :

:

, где  — вероятность наступления события,

— вероятность наступления события,  — вероятность НЕ наступления события

— вероятность НЕ наступления события

Например, если вероятность того, что молодой, сильный и резвый конь по прозвищу «Ветерок» обойдет на скачках старую и дряблую старушку по кличке «Матильда» равняется  , то шансы на успех «Ветерка» составят

, то шансы на успех «Ветерка» составят  к

к  и наоборот, зная шансы, нам не составит труда вычислить вероятность :

и наоборот, зная шансы, нам не составит труда вычислить вероятность :

Таким образом, мы научились «переводить» вероятность в шансы, которые принимают значения от до . Сделаем еще один шаг и научимся «переводить» вероятность на всю числовую прямую от до .

Шаг 2. Переведем значения вероятности в диапазон

Шаг этот очень простой — прологарифмируем шансы по основанию числа Эйлера  и получим:

и получим:

Теперь мы знаем, что если  , то вычислить значение будет очень просто и, более того, оно должно быть положительным:

, то вычислить значение будет очень просто и, более того, оно должно быть положительным:  . Так и есть.

. Так и есть.

Ради любопытства проверим, что если  , тогда мы ожидаем увидеть отрицательное значение . Проверяем:

, тогда мы ожидаем увидеть отрицательное значение . Проверяем:  . Все верно.

. Все верно.

Теперь мы знаем как перевести значение вероятности от до на всю числовую прямую от до . В следующем шаге сделаем все наоборот.

А пока, отметим, что в соответствии с правилами логарифмирования, зная значение функции , можно вычислить шансы:

Этот способ определения шансов нам пригодится на следующем шаге.

Шаг 3. Выведем формулу для определения

Итак, мы научились, зная , находить значения функции . Однако, на самом деле нам нужно все с точностью до наоборот — зная значение находить . Для этого обратимся к такому понятию как обратная функция шансов, в соответствии с которой:

В статье мы не будем выводить вышеобозначенную формулу, но проверим на цифрах из примера выше. Мы знаем, что при шансах равными 4 к 1 ( ), вероятность наступления события равна 0.8 (). Сделаем подстановку:

), вероятность наступления события равна 0.8 (). Сделаем подстановку:  . Это совпадает с нашими вычислениями, проведенными ранее. Двигаемся далее.

. Это совпадает с нашими вычислениями, проведенными ранее. Двигаемся далее.

На прошлом шаге мы вывели, что  , а значит можно сделать замену в обратной функции шансов. Получим:

, а значит можно сделать замену в обратной функции шансов. Получим:

Разделим и числитель и знаменатель на  , тогда:

, тогда:

На всякий пожарный, дабы убедиться, что мы нигде не ошиблись, сделаем еще одну небольшую проверку. На шаге 2, мы для определили, что  . Тогда, подставив значение в функцию логистического отклика, мы ожидаем получить . Подставляем и получаем:

. Тогда, подставив значение в функцию логистического отклика, мы ожидаем получить . Подставляем и получаем:

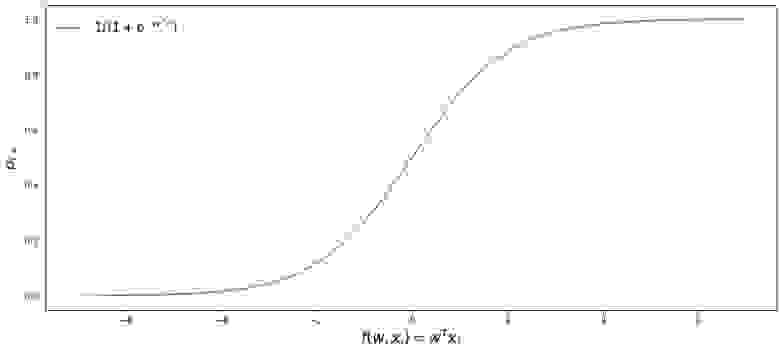

Поздравляю вас, уважаемый читатель, мы только что вывели и протестировали функцию логистического отклика. Давайте посмотрим на график функции.

График 3 «Функция логистического отклика»

Код для отрисовки графика

import math

def logit (f):

return 1/(1+math.exp(-f))

f = np.arange(-7,7,0.05)

p = []

for i in f:

p.append(logit(i))

fig, axes = plt.subplots(figsize = (14,6), dpi = 80)

plt.plot(f, p, color = 'grey', label = '$ 1 / (1+e^{-w^Tx_i})$')

plt.xlabel('$f(w,x_i) = w^Tx_i$', size = 16)

plt.ylabel('$p_{i+}$', size = 16)

plt.legend(prop = {'size': 14})

plt.show()

В литературе также можно встретить название данной функции как сигмоид-функция. По графику хорошо заметно, что основное изменение вероятности принадлежности объекта к классу происходит на относительно небольшом диапазоне , где-то от  до

до  .

.

Предлагаю вернуться к нашему кредитному аналитику и помочь ему с вычислением вероятности погашения кредитов, иначе он рискует остаться без премии

Таблица 2 «Потенциальные заемщики»

Код для формирования таблицы

proba = []

for i in df['f(w,x)']:

proba.append(round(logit(i),2))

df['Probability'] = proba

df[['The borrower', 'Salary', 'Payment', 'f(w,x)', 'Decision', 'Probability']]

Итак, вероятность возврата кредита мы определили. В целом, это похоже на правду.

Действительно, вероятность того что Вася при зарплате в 120.000Р сможет ежемесячно отдавать в банк 3.000Р близка к 100%. Кстати, мы должны понимать, что банк может выдать кредит и Леше в том случае, если политикой банка предусмотрено, например, кредитовать клиентов с вероятностью возврата кредита более, ну скажем, 0.3. Просто в таком случае банк сформирует больший резерв под возможные потери.

Также следует отметить, что соотношение зарплаты к платежу не менее 3 и с запасом в 5.000Р было взято с потолка. Поэтому нам нельзя было использовать в первоначальном виде вектор весов  . Нам требовалось сильно уменьшить коэффициенты и в таком случае мы разделили каждый коэффициент на 25.000, то есть по сути мы подогнали результат. Но это сделано было специально, чтобы упростить понимание материала на начальном этапе. В жизни, же нам потребуется не выдумывать и подгонять коэффициенты, а находить их. Как раз в следующих разделах статьи мы выведем уравнения, с помощью которых подбираются параметры .

. Нам требовалось сильно уменьшить коэффициенты и в таком случае мы разделили каждый коэффициент на 25.000, то есть по сути мы подогнали результат. Но это сделано было специально, чтобы упростить понимание материала на начальном этапе. В жизни, же нам потребуется не выдумывать и подгонять коэффициенты, а находить их. Как раз в следующих разделах статьи мы выведем уравнения, с помощью которых подбираются параметры .

04. Метод наименьших квадратов при определении вектора весов в функции логистического отклика

Нам уже известен такой метод подбора вектора весов , как метод наименьших квадратов (МНК) и собственно, почему бы нам тогда не использовать его в задачах бинарной классификации? Действительно, ничто не мешает использовать МНК, только вот данный способ в задачах классификации дает результаты менее точные, нежели Logistic Loss. Этому есть теоретическое обоснование. Давайте для начала посмотрим на один простой пример.

Предположим, что наши модели (использующие MSE и Logistic Loss) уже начали подбор вектора весов и мы остановили расчет на каком-то шаге. Неважно, в середине, в конце или в начале, главное, что у нас уже есть какие-то значения вектора весов и допустим, что на этом шаге, вектора весов для обеих моделей не имеют различий. Тогда возьмем полученные веса и подставим их в функцию логистического отклика ( ) для какого-нибудь объекта, который относится к классу . Исследуем два случая, когда в соответствии с подобранным вектором весов наша модель сильно ошибается и наоборот — модель сильно уверена в том, что объект относится к классу . Посмотрим какие штрафы будут «выписаны» при использовании МНК и Logistic Loss.

) для какого-нибудь объекта, который относится к классу . Исследуем два случая, когда в соответствии с подобранным вектором весов наша модель сильно ошибается и наоборот — модель сильно уверена в том, что объект относится к классу . Посмотрим какие штрафы будут «выписаны» при использовании МНК и Logistic Loss.

Код для расчета штрафов в зависимости от используемой функции потерь

# класс объекта

y = 1

# вероятность отнесения объекта к классу в соответствии с параметрами w

proba_1 = 0.01

MSE_1 = (y - proba_1)**2

print 'Штраф MSE при грубой ошибке =', MSE_1

# напишем функцию для вычисления f(w,x) при известной вероятности отнесения объекта к классу +1 (f(w,x)=ln(odds+))

def f_w_x(proba):

return math.log(proba/(1-proba))

LogLoss_1 = math.log(1+math.exp(-y*f_w_x(proba_1)))

print 'Штраф Log Loss при грубой ошибке =', LogLoss_1

proba_2 = 0.99

MSE_2 = (y - proba_2)**2

LogLoss_2 = math.log(1+math.exp(-y*f_w_x(proba_2)))

print '**************************************************************'

print 'Штраф MSE при сильной уверенности =', MSE_2

print 'Штраф Log Loss при сильной уверенности =', LogLoss_2

Случай с грубой ошибкой — модель относит объект к классу с вероятностью в 0,01

Штраф при использовании МНК составит:

Штраф при использовании Logistic Loss составит:

Случай с сильной уверенностью — модель относит объект к классу с вероятностью в 0,99

Штраф при использовании МНК составит:

Штраф при использовании Logistic Loss составит:

Этот пример хорошо иллюстрирует, что при грубой ошибке функция потерь Log Loss штрафует модель значительно сильнее, чем MSE. Давайте теперь разберемся, каковы теоретические предпосылки использования функции потерь Log Loss в задачах классификации.

05. Метод максимального правдоподобия и логистическая регрессия

Как и было обещано в начале, статья изобилует простыми примерами. В студии очередной пример и старые гости — заемщики банка: Вася, Федя и Леша.

На всякий пожарный, перед тем как развивать пример, напомню, что в жизни мы имеем дело с обучающей выборкой из тысяч или миллионов объектов с десятками или сотнями признаков. Однако здесь цифры взяты так, чтобы они легко укладывались в голове начинающего датасайнтеста.

Возвращаемся к примеру. Представим, что директор банка решил выдать кредит всем нуждающимся, несмотря на то, что алгоритм подсказывал не выдавать его Леше. И вот прошло достаточно времени и нам стало известно кто из трех героев погасил кредит, а кто нет. Что и следовало ожидать: Вася и Федя погасили кредит, а Леша — нет. Теперь давайте представим, что этот результат будет для нас новой обучающей выборкой и, при этом у нас как будто исчезли все данные о факторах, влияющих на вероятность погашения кредита (зарплата заемщика, размер ежемесячного платежа). Тогда интуитивно мы можем полагать, что каждый третий заемщик не возвращает банку кредит или другими словами вероятность возврата кредита следующим заемщиком  . Этому интуитивному предположению есть теоретическое подтверждение и основывается оно на методе максимального правдоподобия, часто в литературе его называют принципом максимального правдоподобия.

. Этому интуитивному предположению есть теоретическое подтверждение и основывается оно на методе максимального правдоподобия, часто в литературе его называют принципом максимального правдоподобия.

Для начала познакомимся с понятийным аппаратом.

Правдоподобие выборки — это вероятность получения именно такой выборки, получения именно таких наблюдений / результатов, т.е. произведение вероятностей получения каждого из результатов выборки (например, погашен или не погашен кредит Васей, Федей и Лешей одновременно).

Функция правдоподобия связывает правдоподобие выборки со значениями параметров распределения.

В нашем случае, обучающая выборка представляет собой обобщённую схему Бернулли, в которой случайная величина принимает всего два значения: или . Следовательно, правдоподобие выборки можно записать как функцию правдоподобия от параметра  следующим образом:

следующим образом:

Вышеуказанную запись можно интерпретировать так. Совместная вероятность того, что Вася и Федя погасят кредит равна  , вероятность того что Леша НЕ погасит кредит равна

, вероятность того что Леша НЕ погасит кредит равна  (так как имело место именно НЕ погашение кредита), следовательно совместная вероятность всех трех событий равна

(так как имело место именно НЕ погашение кредита), следовательно совместная вероятность всех трех событий равна  .

.

Метод максимального правдоподобия — это метод оценки неизвестного параметра путём максимизации функции правдоподобия. В нашем случае требуется найти такое значение , при котором  достигает максимума.

достигает максимума.

Откуда собственно идея – искать значение неизвестного параметра, при котором функция правдоподобия достигает максимума? Истоки идеи проистекают из представления о том, что выборка – это единственный, доступный нам, источник знания о генеральной совокупности. Все, что нам известно о генеральной совокупности, представлено в выборке. Поэтому, все, что мы можем сказать, так это то, что выборка – это наиболее точное отражение генеральной совокупности, доступное нам. Следовательно, нам требуется найти такой параметр, при котором имеющаяся выборка становится наиболее вероятной.

Очевидно, мы имеем дело с оптимизационной задачей, в которой требуется найти точку экстремума функции. Для нахождения точки экстремума необходимо рассмотреть условие первого порядка, то есть приравнять производную функции к нулю и решить уравнение относительно искомого параметра. Однако поиски производной произведения большого количества множителей могут оказаться делом затяжным, чтобы этого избежать существует специальный прием — переход к логарифму функции правдоподобия. Почему возможен такой переход? Обратим внимание на то, что мы ищем не сам экстремум функции , а точку экстремума, то есть то значение неизвестного параметра , при котором достигает максимума. При переходе к логарифму точка экстремума не меняется (хотя сам экстремум будет отличаться), так как логарифм — монотонная функция.

, а точку экстремума, то есть то значение неизвестного параметра , при котором достигает максимума. При переходе к логарифму точка экстремума не меняется (хотя сам экстремум будет отличаться), так как логарифм — монотонная функция.

Давайте, в соответствии с вышеизложенным, продолжим развивать наш пример с кредитами у Васи, Феди и Леши. Для начала перейдем к логарифму функции правдоподобия:

Теперь мы можем с легкостью продифференцировать выражение по :

И наконец, рассмотрим условие первого порядка — приравняем производную функции к нулю:

Таким образом, наша интуитивная оценка вероятности погашения кредита была теоретически обоснована.

Отлично, но что нам теперь делать с такой информацией? Если мы будем считать, что каждый третий заемщик не вернет банку деньги, то последний неизбежно разорится. Так-то оно так, да только при оценке вероятности погашения кредита равной  мы не учли факторы, влияющие на возврат кредита: заработная плата заемщика и размер ежемесячного платежа. Вспомним, что ранее мы рассчитали вероятность возврата кредита каждым клиентом с учетом этих самых факторов. Логично, что и вероятности у нас получились отличные от константы равной .

мы не учли факторы, влияющие на возврат кредита: заработная плата заемщика и размер ежемесячного платежа. Вспомним, что ранее мы рассчитали вероятность возврата кредита каждым клиентом с учетом этих самых факторов. Логично, что и вероятности у нас получились отличные от константы равной .

Давайте определим правдоподобие выборок:

Код для расчетов правдоподобий выборок

from functools import reduce

def likelihood(y,p):

line_true_proba = []

for i in range(len(y)):

ltp_i = p[i]**y[i]*(1-p[i])**(1-y[i])

line_true_proba.append(ltp_i)

likelihood = []

return reduce(lambda a, b: a*b, line_true_proba)

y = [1.0,1.0,0.0]

p_log_response = df['Probability']

const = 2.0/3.0

p_const = [const, const, const]

print 'Правдоподобие выборки при константном значении p=2/3:', round(likelihood(y,p_const),3)

print '****************************************************************************************************'

print 'Правдоподобие выборки при расчетном значении p:', round(likelihood(y,p_log_response),3)

Правдоподобие выборки при константном значении :

Правдоподобие выборки при расчете вероятности погашения кредита с учетом факторов  :

:

Правдоподобие выборки с вероятностью, посчитанной в зависимости от факторов оказалось выше правдоподобия при константном значении вероятности. О чем это говорит? Это говорит о том, что знания о факторах позволили подобрать более точно вероятность погашения кредита для каждого клиента. Поэтому, при выдаче очередного кредита, правильнее будет использовать, предложенную в конце 3-го раздела статьи, модель оценки вероятности погашения задолженности.

Но тогда, если нам требуется максимизировать функцию правдоподобия выборки, то почему бы не использовать какой-нибудь алгоритм, который будет выдавать вероятности для Васи, Феди и Леши, например, равными 0.99, 0.99 и 0.01 соответственно. Возможно такой алгоритм и хорошо себя проявит на обучающей выборке, так как приблизит значение правдоподобия выборки к , но, во-первых, у такого алгоритма будут, скорее всего трудности с обобщающей способностью, во-вторых, этот алгоритм будет точно не линейным. И если, методы борьбы с переобучением (равно слабая обобщающая способность) явно не входят в план этой статьи, то по второму пункту давайте пройдемся подробнее. Для этого, достаточно ответить на простой вопрос. Может ли вероятность погашения кредита Васей и Федей быть одинаковой с учетом известных нам факторов? С точки зрения здравой логики конечно же нет, не может. Так на погашение кредита Вася будет отдавать 2.5% своей зарплаты в месяц, а Федя — почти 27,8%. Также на графике 2 «Классификация клиентов» мы видим, что Вася находится значительно дальше от линии, разделяющей классы, чем Федя. Ну и наконец, мы знаем, что функция  для Васи и Феди принимает различные значения: 4.24 для Васи и 1.0 для Феди. Вот если бы Федя, например, зарабатывал на порядок больше или кредит поменьше просил, то тогда вероятности погашения кредита у Васи и Феди были бы схожими. Другими словами, линейную зависимость не обманешь. И если бы мы действительно рассчитали коэффициенты , а не взяли их с потолка, то могли бы смело заявить, что наши значения лучше всего позволяют оценить вероятность погашения кредита каждым заемщиком, но так как мы условились считать, что определение коэффициентов было проведено по всем правилам, то мы так и будем считать — наши коэффициенты позволяют дать лучшую оценку вероятности

для Васи и Феди принимает различные значения: 4.24 для Васи и 1.0 для Феди. Вот если бы Федя, например, зарабатывал на порядок больше или кредит поменьше просил, то тогда вероятности погашения кредита у Васи и Феди были бы схожими. Другими словами, линейную зависимость не обманешь. И если бы мы действительно рассчитали коэффициенты , а не взяли их с потолка, то могли бы смело заявить, что наши значения лучше всего позволяют оценить вероятность погашения кредита каждым заемщиком, но так как мы условились считать, что определение коэффициентов было проведено по всем правилам, то мы так и будем считать — наши коэффициенты позволяют дать лучшую оценку вероятности

Однако мы отвлеклись. В этом разделе нам надо разобраться как определяется вектор весов , который необходим для оценки вероятности возврата кредита каждым заемщиком.

Кратко резюмируем, с каким арсеналом мы выступаем на поиски коэффициентов :

1. Мы предполагаем, что зависимость между целевой переменной (прогнозным значением) и фактором, оказывающим влияние на результат — линейная. По этой причине применяется функция линейной регрессии вида  , линия которого делит объекты (клиентов) на классы и или (клиенты, способные погасить кредит и не способные). В нашем случае уравнение имеет вид .

, линия которого делит объекты (клиентов) на классы и или (клиенты, способные погасить кредит и не способные). В нашем случае уравнение имеет вид .

2. Мы используем функцию обратного логит-преобразования вида для определения вероятности принадлежности объекта к классу .

3. Мы рассматриваем нашу обучающую выборку как реализацию обобщенной схемы Бернулли, то есть для каждого объекта генерируется случайная величина, которая с вероятностью (своей для каждого объекта) принимает значение 1 и с вероятностью  – 0.

– 0.

4. Мы знаем, что нам требуется максимизировать функцию правдоподобия выборки с учетом принятых факторов для того, чтобы имеющаяся выборка стала наиболее правдоподобной. Другими словами, нам нужно подобрать такие параметры, при которых выборка будет наиболее правдоподобной. В нашем случае подбираемый параметр — это вероятность погашения кредита , которая в свою очередь зависит от неизвестных коэффициентов . Значит нам требуется найти такой вектор весов , при котором правдоподобие выборки будет максимальным.

5. Мы знаем, что для максимизации функции правдоподобия выборки можно использовать метод максимального правдоподобия. И мы знаем все хитрые приемы для работы с этим методом.

Вот такая многоходовочка получается

А теперь вспомним, что в самом начале статьи мы хотели вывести два вида функции потерь Logistic Loss в зависимости от того как обозначаются классы объектов. Так повелось, что в задачах классификации с двумя классами, классы обозначают как и или . В зависимости от обозначения, на выходе будет соответствующая функция потерь.

Случай 1. Классификация объектов на и

Раннее, при определении правдоподобия выборки, в котором вероятность погашения задолженности заемщиком рассчитывалась исходя из факторов и заданных коэффициентов , мы применили формулу:

На самом деле  — это значение функции логистического отклика при заданном векторе весов

— это значение функции логистического отклика при заданном векторе весов

Тогда нам ничто не мешает записать функцию правдоподобия выборки так:

Бывает так, что иногда, некоторым начинающим аналитикам сложно сходу понять, как эта функция работает. Давайте рассмотрим 4 коротких примера, которые все прояснят:

1. Если  (т.е. в соответствии с обучающей выборкой объект относится к классу +1), а наш алгоритм

(т.е. в соответствии с обучающей выборкой объект относится к классу +1), а наш алгоритм  определяет вероятность отнесения объекта к классу равной 0.9, то вот этот кусочек правдоподобия выборки будет рассчитываться так:

определяет вероятность отнесения объекта к классу равной 0.9, то вот этот кусочек правдоподобия выборки будет рассчитываться так:

2. Если , а  , то расчет будет таким:

, то расчет будет таким:

3. Если  , а , то расчет будет таким:

, а , то расчет будет таким:

4. Если , а  , то расчет будет таким:

, то расчет будет таким:

Очевидно, что функция правдоподобия будет максимизироваться в случаях 1 и 3 или в общем случае — при правильно отгаданных значениях вероятностей отнесения объекта к классу .

В связи с тем, что при определении вероятности отнесения объекта к классу нам не известны только коэффициенты , то мы их и будем искать. Как и говорилось выше, это задача оптимизации, в которой для начала нам требуется найти производную от функции правдоподобия по вектору весов . Однако предварительно имеет смысл упростить себе задачу: производную будем искать от логарифма функции правдоподобия.

Почему после логарифмирования, в функции логистической ошибки, мы поменяли знак с  на

на  . Все просто, так как в задачах оценки качества модели принято минимизировать значение функции, то мы умножили правую часть выражения на и соответственно вместо максимизации, теперь минимизируем функцию.

. Все просто, так как в задачах оценки качества модели принято минимизировать значение функции, то мы умножили правую часть выражения на и соответственно вместо максимизации, теперь минимизируем функцию.

Собственно, сейчас, на ваших глазах была много страдальчески выведена функция потерь — Logistic Loss для обучающей выборки с двумя классами: и .

Теперь, для нахождения коэффициентов, нам потребуется всего лишь найти производную функции логистической ошибки и далее, используя численные методы оптимизации, такие как градиентный спуск или стохастический градиентный спуск, подобрать наиболее оптимальные коэффициенты . Но, учитывая, уже не малый объем статьи, предлагается провести дифференцирование самостоятельно или, быть может, это будет темой для следующей статьи с большим количеством арифметики без столь подробных примеров.

Случай 2. Классификация объектов на и

Подход здесь будет такой же, как и с классами и , но сама дорожка к выводу функции потерь Logistic Loss, будет более витиеватой. Приступаем. Будем для функции правдоподобия использовать оператор «если…, то…». То есть, если -ый объект относится к классу , то для расчета правдоподобия выборки используем вероятность , если объект относится к классу , то в правдоподобие подставляем  . Вот так выглядит функция правдоподобия:

. Вот так выглядит функция правдоподобия:

![$P(\mkern 5mu \vec{y} \mkern 5mu |\mkern 5mu \sigma(\vec{w}^TX)) \mkern 5mu = \mkern 5mu \prod\limits_{i=1}^n \sigma(\vec{w}^T\vec{x_i})^{[y_i=+1]} \mkern 10mu (1-\sigma(\vec{w}^T\vec{x_i})^{[y_i=-1])} \mkern 10mu \rightarrow \mkern 10mu max$](https://habrastorage.org/getpro/habr/formulas/4a1/375/d87/4a1375d876abb71c1dd376a63d13c727.svg)

На пальцах распишем как это работает. Рассмотрим 4 случая:

1. Если и  , то в правдоподобие выборки «пойдет»

, то в правдоподобие выборки «пойдет»

2. Если и  , то в правдоподобие выборки «пойдет»

, то в правдоподобие выборки «пойдет»

3. Если  и , то в правдоподобие выборки «пойдет»

и , то в правдоподобие выборки «пойдет»

4. Если и , то в правдоподобие выборки «пойдет»

Очевидно, что в 1 и 3 случае, когда вероятности были правильно определены алгоритмом, функция правдоподобия будет максимизироваться, то есть именно это мы и хотели получить. Однако, такой подход достаточно громоздок и далее мы рассмотрим более компактную запись. Но для начала, логарифмируем функцию правдоподобия с заменой знака, так как теперь мы будем минимизировать ее.

![$L_{log}(X,\vec{y},\vec{w}) = \sum\limits_{i=1}^n(-[y_i=+1] \mkern 2mu log_e \mkern 5mu \sigma(\vec{w}^T \vec{x_i}) - [y_i=-1] \mkern 2mu log_e \mkern 5mu (1 - \sigma(\vec{w}^T \vec{x_i})) ) \rightarrow min$](https://habrastorage.org/getpro/habr/formulas/130/e8f/691/130e8f691883e01464d6cff33b3855b8.svg)

Подставим вместо  выражение

выражение  :

:

![$L_{log}(X,\vec{y},\vec{w}) = \sum\limits_{i=1}^n(-[y_i=+1] \mkern 2mu log_e \mkern 5mu (\frac{1}{1+e^{-\vec{w}^T\vec{x_i}}}) - [y_i=-1] \mkern 2mu log_e \mkern 5mu (1 - \frac{1}{1+e^{-\vec{w}^T\vec{x_i}}})) \rightarrow min$](https://habrastorage.org/getpro/habr/formulas/c2c/0ab/36e/c2c0ab36e7845ed6bc08f3bfa7f7a6f5.svg)

Упростим правое слагаемое под логарифмом, используя простые арифметические приемы и получим:

![$L_{log}(X,\vec{y},\vec{w}) = \sum\limits_{i=1}^n(-[y_i=+1] \mkern 2mu log_e \mkern 5mu (\frac{1}{1+e^{-\vec{w}^T\vec{x_i}}}) - [y_i=-1] \mkern 2mu log_e \mkern 5mu (\frac{1}{1+e^{\vec{w}^T\vec{x_i}}})) \rightarrow min$](https://habrastorage.org/getpro/habr/formulas/c5e/32f/f29/c5e32ff297d5114261c85aa8b00d74e4.svg)

А теперь настало время избавиться от оператора «если…, то…». Заметим, что когда объект  относится к классу , то в выражении под логарифмом, в знаменателе, возводится в степень

относится к классу , то в выражении под логарифмом, в знаменателе, возводится в степень  , если объект относится к классу , то $e$ возводится в степень

, если объект относится к классу , то $e$ возводится в степень  . Следовательно запись степени можно упростить — объединить оба случая в один:

. Следовательно запись степени можно упростить — объединить оба случая в один:  . Тогда функция логистической ошибки примет вид:

. Тогда функция логистической ошибки примет вид:

В соответствии с правилами логарифмирования, перевернем дробь и вынесем знак «» (минус) за логарифм, получим:

Перед вами функция потерь logistic Loss, которая применяется в обучающей выборке с объектами относимых к классам: и .

Что ж, на этом моменте я откланиваюсь и мы завершаем статью.

Предыдущая работа автора — «Приводим уравнение линейной регрессии в матричный вид»

Предыдущая работа автора — «Приводим уравнение линейной регрессии в матричный вид»

Вспомогательные материалы

1. Литература

1) Прикладной регрессионный анализ / Н. Дрейпер, Г. Смит – 2-е изд. – М.: Финансы и статистика, 1986 (перевод с английского)

2) Теория вероятностей и математическая статистика / В.Е. Гмурман — 9-е изд. — М.: Высшая школа, 2003

3) Теория вероятностей / Н.И. Чернова — Новосибирск: Новосибирский государственный университет, 2007

4) Бизнес-аналитика: от данных к знаниям / Паклин Н. Б., Орешков В. И. — 2-е изд. — Санкт-Петербург: Питер, 2013

5) Data Science Наука о данных с нуля / Джоэл Грас — Санкт-Петербург: БХВ Петербург, 2017

6) Практическая статистика для специалистов Data Science / П.Брюс, Э.Брюс — Санкт-Петербург: БХВ Петербург, 2018

2. Лекции, курсы (видео)

1) Суть метода максимального правдоподобия, Борис Демешев

2) Метод максимального правдоподобия в непрерывном случае, Борис Демешев

3) Логистическая регрессия. Открытый курс ODS, Yury Kashnitsky

4) Лекция 4, Евгений Соколов (с 47 минуты видео)

5) Логистическая регрессия, Вячеслав Воронцов

3. Интернет-источники

1) Линейные модели классификации и регрессии

2) Как легко понять логистическую регрессию

3) Логистическая функция ошибки

4) Независимые испытания и формула Бернули

5) Баллада о ММП

6) Метод максимального правдоподобия

7) Формулы и свойства логарифмов

Почему число ?

Почему число ?

9) Линейный классификатор

9) Jupyter notebook на гитхабе

«Logit model» redirects here. Not to be confused with Logit function.

In statistics, the logistic model (or logit model) is a statistical model that models the probability of an event taking place by having the log-odds for the event be a linear combination of one or more independent variables. In regression analysis, logistic regression[1] (or logit regression) is estimating the parameters of a logistic model (the coefficients in the linear combination). Formally, in binary logistic regression there is a single binary dependent variable, coded by an indicator variable, where the two values are labeled «0» and «1», while the independent variables can each be a binary variable (two classes, coded by an indicator variable) or a continuous variable (any real value). The corresponding probability of the value labeled «1» can vary between 0 (certainly the value «0») and 1 (certainly the value «1»), hence the labeling;[2] the function that converts log-odds to probability is the logistic function, hence the name. The unit of measurement for the log-odds scale is called a logit, from logistic unit, hence the alternative names. See § Background and § Definition for formal mathematics, and § Example for a worked example.

Binary variables are widely used in statistics to model the probability of a certain class or event taking place, such as the probability of a team winning, of a patient being healthy, etc. (see § Applications), and the logistic model has been the most commonly used model for binary regression since about 1970.[3] Binary variables can be generalized to categorical variables when there are more than two possible values (e.g. whether an image is of a cat, dog, lion, etc.), and the binary logistic regression generalized to multinomial logistic regression. If the multiple categories are ordered, one can use the ordinal logistic regression (for example the proportional odds ordinal logistic model[4]). See § Extensions for further extensions. The logistic regression model itself simply models probability of output in terms of input and does not perform statistical classification (it is not a classifier), though it can be used to make a classifier, for instance by choosing a cutoff value and classifying inputs with probability greater than the cutoff as one class, below the cutoff as the other; this is a common way to make a binary classifier.

Analogous linear models for binary variables with a different sigmoid function instead of the logistic function (to convert the linear combination to a probability) can also be used, most notably the probit model; see § Alternatives. The defining characteristic of the logistic model is that increasing one of the independent variables multiplicatively scales the odds of the given outcome at a constant rate, with each independent variable having its own parameter; for a binary dependent variable this generalizes the odds ratio. More abstractly, the logistic function is the natural parameter for the Bernoulli distribution, and in this sense is the «simplest» way to convert a real number to a probability. In particular, it maximizes entropy (minimizes added information), and in this sense makes the fewest assumptions of the data being modeled; see § Maximum entropy.

The parameters of a logistic regression are most commonly estimated by maximum-likelihood estimation (MLE). This does not have a closed-form expression, unlike linear least squares; see § Model fitting. Logistic regression by MLE plays a similarly basic role for binary or categorical responses as linear regression by ordinary least squares (OLS) plays for scalar responses: it is a simple, well-analyzed baseline model; see § Comparison with linear regression for discussion. The logistic regression as a general statistical model was originally developed and popularized primarily by Joseph Berkson,[5] beginning in Berkson (1944), where he coined «logit»; see § History.

Applications[edit]

Logistic regression is used in various fields, including machine learning, most medical fields, and social sciences. For example, the Trauma and Injury Severity Score (TRISS), which is widely used to predict mortality in injured patients, was originally developed by Boyd et al. using logistic regression.[6] Many other medical scales used to assess severity of a patient have been developed using logistic regression.[7][8][9][10] Logistic regression may be used to predict the risk of developing a given disease (e.g. diabetes; coronary heart disease), based on observed characteristics of the patient (age, sex, body mass index, results of various blood tests, etc.).[11][12] Another example might be to predict whether a Nepalese voter will vote Nepali Congress or Communist Party of Nepal or Any Other Party, based on age, income, sex, race, state of residence, votes in previous elections, etc.[13] The technique can also be used in engineering, especially for predicting the probability of failure of a given process, system or product.[14][15] It is also used in marketing applications such as prediction of a customer’s propensity to purchase a product or halt a subscription, etc.[16] In economics, it can be used to predict the likelihood of a person ending up in the labor force, and a business application would be to predict the likelihood of a homeowner defaulting on a mortgage. Conditional random fields, an extension of logistic regression to sequential data, are used in natural language processing.

Example[edit]

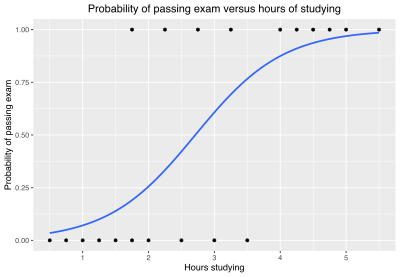

Problem[edit]

As a simple example, we can use a logistic regression with one explanatory variable and two categories to answer the following question:

A group of 20 students spends between 0 and 6 hours studying for an exam. How does the number of hours spent studying affect the probability of the student passing the exam?

The reason for using logistic regression for this problem is that the values of the dependent variable, pass and fail, while represented by «1» and «0», are not cardinal numbers. If the problem was changed so that pass/fail was replaced with the grade 0–100 (cardinal numbers), then simple regression analysis could be used.

The table shows the number of hours each student spent studying, and whether they passed (1) or failed (0).

| Hours (xk) | 0.50 | 0.75 | 1.00 | 1.25 | 1.50 | 1.75 | 1.75 | 2.00 | 2.25 | 2.50 | 2.75 | 3.00 | 3.25 | 3.50 | 4.00 | 4.25 | 4.50 | 4.75 | 5.00 | 5.50 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Pass (yk) | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 1 | 0 | 1 | 0 | 1 | 1 | 1 | 1 | 1 | 1 |

We wish to fit a logistic function to the data consisting of the hours studied (xk) and the outcome of the test (yk =1 for pass, 0 for fail). The data points are indexed by the subscript k which runs from  to

to  . The x variable is called the «explanatory variable», and the y variable is called the «categorical variable» consisting of two categories: «pass» or «fail» corresponding to the categorical values 1 and 0 respectively.

. The x variable is called the «explanatory variable», and the y variable is called the «categorical variable» consisting of two categories: «pass» or «fail» corresponding to the categorical values 1 and 0 respectively.

Model[edit]

The logistic function is of the form:

where μ is a location parameter (the midpoint of the curve, where  ) and s is a scale parameter. This expression may be rewritten as:

) and s is a scale parameter. This expression may be rewritten as:

where  and is known as the intercept (it is the vertical intercept or y-intercept of the line

and is known as the intercept (it is the vertical intercept or y-intercept of the line  ), and

), and  (inverse scale parameter or rate parameter): these are the y-intercept and slope of the log-odds as a function of x. Conversely,

(inverse scale parameter or rate parameter): these are the y-intercept and slope of the log-odds as a function of x. Conversely,  and

and  .

.

Fit[edit]

The usual measure of goodness of fit for a logistic regression uses logistic loss (or log loss), the negative log-likelihood. For a given xk and yk, write  . The

. The  are the probabilities that the corresponding

are the probabilities that the corresponding  will be unity and

will be unity and  are the probabilities that they will be zero (see Bernoulli distribution). We wish to find the values of

are the probabilities that they will be zero (see Bernoulli distribution). We wish to find the values of  and

and  which give the «best fit» to the data. In the case of linear regression, the sum of the squared deviations of the fit from the data points (yk), the squared error loss, is taken as a measure of the goodness of fit, and the best fit is obtained when that function is minimized.

which give the «best fit» to the data. In the case of linear regression, the sum of the squared deviations of the fit from the data points (yk), the squared error loss, is taken as a measure of the goodness of fit, and the best fit is obtained when that function is minimized.

The log loss for the k-th point is:

The log loss can be interpreted as the «surprisal» of the actual outcome relative to the prediction , and is a measure of information content. Note that log loss is always greater than or equal to 0, equals 0 only in case of a perfect prediction (i.e., when  and

and  , or

, or  and

and  ), and approaches infinity as the prediction gets worse (i.e., when and

), and approaches infinity as the prediction gets worse (i.e., when and  or and

or and  ), meaning the actual outcome is «more surprising». Since the value of the logistic function is always strictly between zero and one, the log loss is always greater than zero and less than infinity. Note that unlike in a linear regression, where the model can have zero loss at a point by passing through a data point (and zero loss overall if all points are on a line), in a logistic regression it is not possible to have zero loss at any points, since is either 0 or 1, but

), meaning the actual outcome is «more surprising». Since the value of the logistic function is always strictly between zero and one, the log loss is always greater than zero and less than infinity. Note that unlike in a linear regression, where the model can have zero loss at a point by passing through a data point (and zero loss overall if all points are on a line), in a logistic regression it is not possible to have zero loss at any points, since is either 0 or 1, but  .

.

These can be combined into a single expression:

This expression is more formally known as the cross-entropy of the predicted distribution  from the actual distribution

from the actual distribution  , as probability distributions on the two-element space of (pass, fail).

, as probability distributions on the two-element space of (pass, fail).

The sum of these, the total loss, is the overall negative log-likelihood  , and the best fit is obtained for those choices of and for which is minimized.

, and the best fit is obtained for those choices of and for which is minimized.

Alternatively, instead of minimizing the loss, one can maximize its inverse, the (positive) log-likelihood:

or equivalently maximize the likelihood function itself, which is the probability that the given data set is produced by a particular logistic function:

This method is known as maximum likelihood estimation.

Parameter estimation[edit]

Since ℓ is nonlinear in and , determining their optimum values will require numerical methods. Note that one method of maximizing ℓ is to require the derivatives of ℓ with respect to and to be zero:

and the maximization procedure can be accomplished by solving the above two equations for and , which, again, will generally require the use of numerical methods.

The values of and which maximize ℓ and L using the above data are found to be:

which yields a value for μ and s of:

Predictions[edit]

The and coefficients may be entered into the logistic regression equation to estimate the probability of passing the exam.

For example, for a student who studies 2 hours, entering the value  into the equation gives the estimated probability of passing the exam of 0.25:

into the equation gives the estimated probability of passing the exam of 0.25:

Similarly, for a student who studies 4 hours, the estimated probability of passing the exam is 0.87:

This table shows the estimated probability of passing the exam for several values of hours studying.

| Hours of study (x) |

Passing exam | ||

|---|---|---|---|

| Log-odds (t) | Odds (et) | Probability (p) | |

| 1 | −2.57 | 0.076 ≈ 1:13.1 | 0.07 |

| 2 | −1.07 | 0.34 ≈ 1:2.91 | 0.26 |

|

0 | 1 |  = 0.50 = 0.50

|

| 3 | 0.44 | 1.55 | 0.61 |

| 4 | 1.94 | 6.96 | 0.87 |

| 5 | 3.45 | 31.4 | 0.97 |

Model evaluation[edit]

The logistic regression analysis gives the following output.

| Coefficient | Std. Error | z-value | p-value (Wald) | |

|---|---|---|---|---|

| Intercept (β0) | −4.1 | 1.8 | −2.3 | 0.021 |

| Hours (β1) | 1.5 | 0.6 | 2.4 | 0.017 |

By the Wald test, the output indicates that hours studying is significantly associated with the probability of passing the exam ( ). Rather than the Wald method, the recommended method[citation needed] to calculate the p-value for logistic regression is the likelihood-ratio test (LRT), which for these data give

). Rather than the Wald method, the recommended method[citation needed] to calculate the p-value for logistic regression is the likelihood-ratio test (LRT), which for these data give  (see § Deviance and likelihood ratio tests below).

(see § Deviance and likelihood ratio tests below).

Generalizations[edit]

This simple model is an example of binary logistic regression, and has one explanatory variable and a binary categorical variable which can assume one of two categorical values. Multinomial logistic regression is the generalization of binary logistic regression to include any number of explanatory variables and any number of categories.

Background[edit]

; note that

; note that  for all

for all  .

.

Definition of the logistic function[edit]

An explanation of logistic regression can begin with an explanation of the standard logistic function. The logistic function is a sigmoid function, which takes any real input , and outputs a value between zero and one.[2] For the logit, this is interpreted as taking input log-odds and having output probability. The standard logistic function  is defined as follows:

is defined as follows:

A graph of the logistic function on the t-interval (−6,6) is shown in Figure 1.

Let us assume that is a linear function of a single explanatory variable  (the case where is a linear combination of multiple explanatory variables is treated similarly). We can then express as follows:

(the case where is a linear combination of multiple explanatory variables is treated similarly). We can then express as follows:

And the general logistic function  can now be written as:

can now be written as:

In the logistic model,  is interpreted as the probability of the dependent variable

is interpreted as the probability of the dependent variable  equaling a success/case rather than a failure/non-case. It is clear that the response variables

equaling a success/case rather than a failure/non-case. It is clear that the response variables  are not identically distributed:

are not identically distributed:  differs from one data point

differs from one data point  to another, though they are independent given design matrix

to another, though they are independent given design matrix  and shared parameters

and shared parameters  .[11]

.[11]

Definition of the inverse of the logistic function[edit]

We can now define the logit (log odds) function as the inverse  of the standard logistic function. It is easy to see that it satisfies:

of the standard logistic function. It is easy to see that it satisfies:

and equivalently, after exponentiating both sides we have the odds:

Interpretation of these terms[edit]

In the above equations, the terms are as follows:

Definition of the odds[edit]

The odds of the dependent variable equaling a case (given some linear combination of the predictors) is equivalent to the exponential function of the linear regression expression. This illustrates how the logit serves as a link function between the probability and the linear regression expression. Given that the logit ranges between negative and positive infinity, it provides an adequate criterion upon which to conduct linear regression and the logit is easily converted back into the odds.[2]

So we define odds of the dependent variable equaling a case (given some linear combination of the predictors) as follows:

The odds ratio[edit]

For a continuous independent variable the odds ratio can be defined as:

The image represents an outline of what an odds ratio looks like in writing, through a template in addition to the test score example in the «Example» section of the contents. In simple terms, if we hypothetically get an odds ratio of 2 to 1, we can say… «For every one-unit increase in hours studied, the odds of passing (group 1) or failing (group 0) are (expectedly) 2 to 1 (Denis, 2019).

This exponential relationship provides an interpretation for : The odds multiply by  for every 1-unit increase in x.[17]

for every 1-unit increase in x.[17]

For a binary independent variable the odds ratio is defined as  where a, b, c and d are cells in a 2×2 contingency table.[18]

where a, b, c and d are cells in a 2×2 contingency table.[18]

Multiple explanatory variables[edit]

If there are multiple explanatory variables, the above expression  can be revised to

can be revised to  . Then when this is used in the equation relating the log odds of a success to the values of the predictors, the linear regression will be a multiple regression with m explanators; the parameters

. Then when this is used in the equation relating the log odds of a success to the values of the predictors, the linear regression will be a multiple regression with m explanators; the parameters  for all

for all  are all estimated.

are all estimated.

Again, the more traditional equations are:

and

where usually  .

.

Definition[edit]

The basic setup of logistic regression is as follows. We are given a dataset containing N points. Each point i consists of a set of m input variables x1,i … xm,i (also called independent variables, explanatory variables, predictor variables, features, or attributes), and a binary outcome variable Yi (also known as a dependent variable, response variable, output variable, or class), i.e. it can assume only the two possible values 0 (often meaning «no» or «failure») or 1 (often meaning «yes» or «success»). The goal of logistic regression is to use the dataset to create a predictive model of the outcome variable.

As in linear regression, the outcome variables Yi are assumed to depend on the explanatory variables x1,i … xm,i.

- Explanatory variables

The explanatory variables may be of any type: real-valued, binary, categorical, etc. The main distinction is between continuous variables and discrete variables.

(Discrete variables referring to more than two possible choices are typically coded using dummy variables (or indicator variables), that is, separate explanatory variables taking the value 0 or 1 are created for each possible value of the discrete variable, with a 1 meaning «variable does have the given value» and a 0 meaning «variable does not have that value».)

- Outcome variables

Formally, the outcomes Yi are described as being Bernoulli-distributed data, where each outcome is determined by an unobserved probability pi that is specific to the outcome at hand, but related to the explanatory variables. This can be expressed in any of the following equivalent forms:

![{\displaystyle {\begin{aligned}Y_{i}\mid x_{1,i},\ldots ,x_{m,i}\ &\sim \operatorname {Bernoulli} (p_{i})\\\operatorname {\mathbb {E} } [Y_{i}\mid x_{1,i},\ldots ,x_{m,i}]&=p_{i}\\\Pr(Y_{i}=y\mid x_{1,i},\ldots ,x_{m,i})&={\begin{cases}p_{i}&{\text{if }}y=1\\1-p_{i}&{\text{if }}y=0\end{cases}}\\\Pr(Y_{i}=y\mid x_{1,i},\ldots ,x_{m,i})&=p_{i}^{y}(1-p_{i})^{(1-y)}\end{aligned}}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/49627157ac00e729a38538029505c210f99955d7)

The meanings of these four lines are: